The Difference Between an RRSP and a TFSA

Pay tax now or pay tax later? It’s all up to you and how you earn income.

Good morning my dear friends!

Today’s topic is one I absolutely love discussing with clients, simply because it’s such a personal and unique situation for each person. In the same way certain types of exercises or dietary restrictions are important for certain types of people, so too is the recommendation of an RRSP or a TFSA for certain types of earners. There’s no one right answer for anyone, and this makes it all the fun in the world to discuss.

In the meantime, I hope everyone is keeping safe and healthy.

I read an article this week about the smallpox epidemic that raged through Montreal in 1885. Mandatory vaccinations, major restrictions, public labelling of infection — 1885 Montreal had it all. There were public rallies back then, too, and doctors who opposed public health orders, too.

Worst of all, 1 in 50 Montrealers died in 1885 due to smallpox. And 90%+ were children under the age of 20.

History repeating itself. Yet, here we are, thinking we’re in some unique epoch of human history.

I hope everyone is able to stay sane during these interesting times. Hopefully this week’s topic distracts you for a bit from everything happening around you.

Quick Thought of the Week

There’s this growing debate in my area about what is and what is not an essential business or an essential item.

I find it utterly fascinating listening to people debate about the essentialism of certain goods.

Some argue a clothing store shouldn’t be open during this restrictive time. Others argue you should be allowed to sell video game consoles. And through thick and thin, the liquor store is always allowed to be open.

The more I look at the Economic Circle of Life, the more I think every good is essential. If it wasn’t essential, there wouldn’t be a market for it.

Superfluous? Extravagant? Luxurious? Waste of money? Frivolous? Sure. I can accept those adjectives.

But “un-essential”, well, it’s not my place to judge.

Link of the Week: Canadian households and businesses sitting on $170 billion excess cash hoard

This article is utterly fascinating. As it turns out, the Canadian government went on a borrowing spree in the first few months of the COVID-19 pandemic, and many Canadians decided to sock that cash away for a future rainy day.

It’ll be fascinating to see how Canadian individuals and businesses opt to use this $170 billion cash hoard as the pandemic draws (hopefully) draws to a close.

The Difference Between an RRSP and a TFSA

There is one core difference between an RRSP and a TFSA: the timing of tax.

This is fundamental to understanding how a Registered Retirement Savings Plan (RRSP) and Tax-Free Savings Account (TFSA) fit into your long-term retirement planning. One account defers tax until the point of withdrawal while the other requires tax be paid up front in lieu of paying tax on the earnings down the road.

Both accounts are powerful. And if handled correctly, both end up with nearly the same amount of after-tax cash.

...Assuming you’ve handled your tax brackets correctly.

Let’s dive in.

Timing of Tax

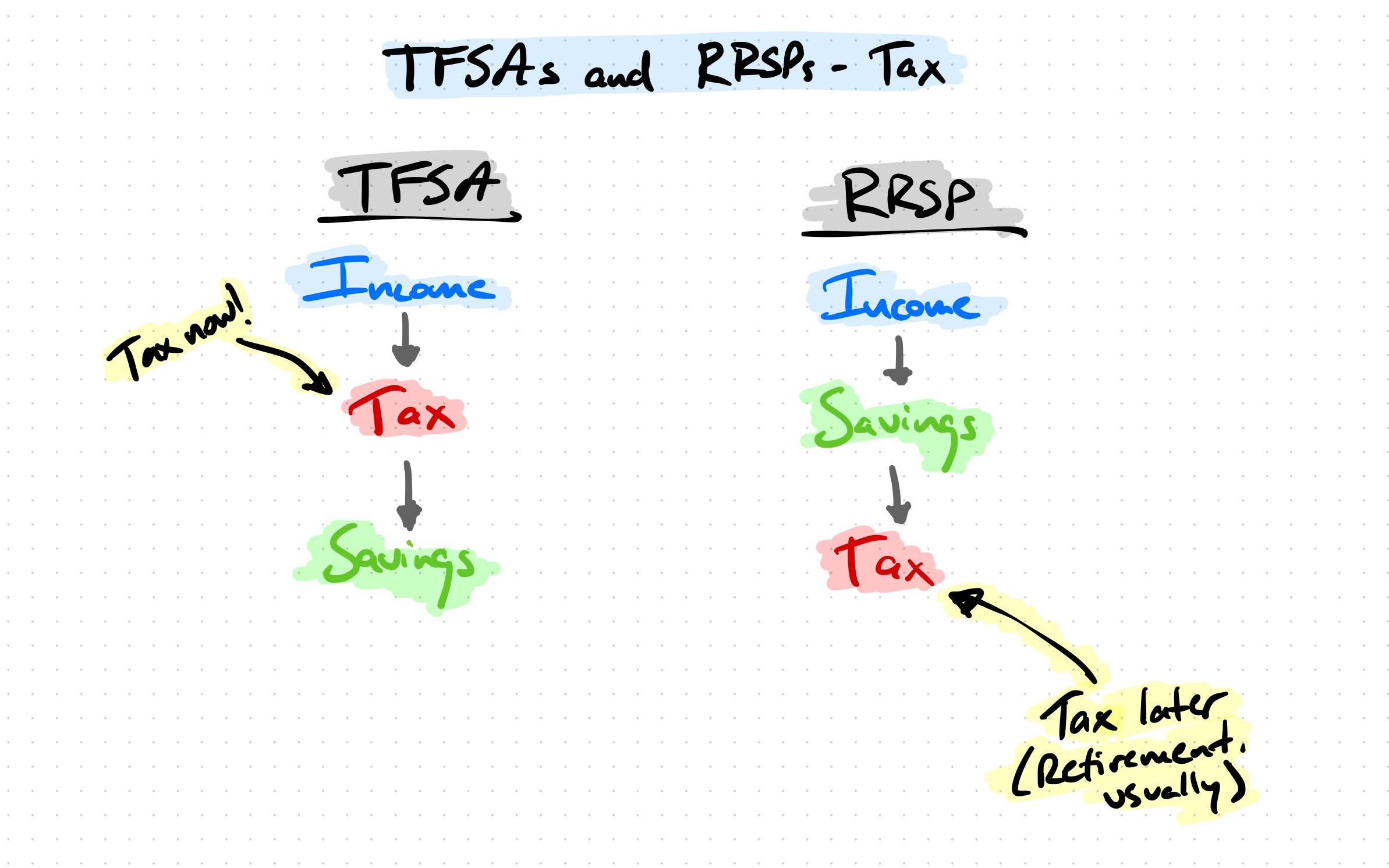

First, take a look at this little drawing I put together. Using the drawing, you can garner a visual of how the two accounts work very differently from one another.

A Tax-Free Savings Account (TFSA) is an after-tax savings account that has tax-free earnings. This means you pay tax on the income amounts you contribute to the account and the subsequent investment earnings in that savings account are tax-free. TFSAs can be used as investment vehicles as well — you can contribute to the TFSA and use the contributions to purchase shares in the stock market, for instance. Interest, dividends, and capital gains on amounts invested in the TFSA are tax-free.

The process flows in the following order:

You earn income (employment, dividends, interest, business income, etc.).

You pay tax on the income (this is done by filing your tax return).

You contribute to your TFSA with your after-tax income.

The TFSA contributions grow tax-free.

You do not pay tax when you withdraw from your TFSA.

Registered Retirement Savings Plans (RRSPs) are the opposite. With an RRSP, you contribute to the plan with pre-tax income. The contributions can be put into a savings account where you earn interest, or like a TFSA, they can be used to invest in the stock, bond, or other markets. The earnings on the amounts invested are tax-free. However, when you go to withdraw funds from your RRSP, you will pay tax on your withdrawals.

The process works something like this:

You earn income (employment, dividends, interest, business income, etc.)

You contribute to your RRSP with your income.

You receive a deduction on your tax return for the amounts contributed to your RRSP. This usually generates a refund on your tax return.

The RRSP contributions grow tax-free.

You pay tax when you withdraw from your RRSP.

There are a bunch of other intricacies to learn about TFSAs and RRSPs (namely around contribution thresholds, how foreign dividends and interest are handled, and how to contribute to your RRSP pre-payroll deductions), but this is the core difference between the two savings plans.

Tax is paid now in a TFSA.

Tax is paid later in an RRSP.

Maximizing the Amounts in Each Account

How you achieve the maximum amount in each account and pay the most efficient amount of tax in each account is entirely dependent on your income makeup and your long-term plans. It’s also dependent on future tax rates, which seem destined for new heights given the loads of take the Canadian government has taken on. As such, it’s very difficult to perfectly measure the maximum amount you can earn inside each account.

There are, of course, rules of thumb.

If you expect to earn less per year in the future than you do right now, it’s generally advisable to contribute to an RRSP.

If you expect your earnings to stay relatively stable throughout your life, it’s generally advisable to contribute to a TFSA.

RRSPs grow with a larger amount of initial contribution (assuming you contribute the refund generated by the RRSP deduction). And if you’re quick on the draw when it comes to exponential growth rates and compound interest, you’ll quickly realize you can amass a far larger amount in the same amount of time at the same earnings rates if you start with a larger amount at the start.

But you’ll pay tax down the road.

For a TFSA, you start with a smaller initial principal amount, but the earnings aren’t taxed down the road.So while your compounded growth is going to be slower and smaller, there’s no future amount you have to give up when you withdraw.

An example:

You make $1,000 and contribute the $1,000 to your RRSP. It grows at 5%, compounded monthly, for 30 years into an amount of $4,467. You withdraw the amount and will likely pay around 25% tax at that time, leaving you with $3,350 of after-tax income.

You make $1,000 and contribute $750 to your TFSA because you had to pay 25% tax up-front. It grows at 5%, compounded monthly, for 30 years into an amount of $3,350. You do not pay tax on that amount when you withdraw it.

Same. Exact. Amount. Of after-tax income.

Note that you must contribute your generated refund into the RRSP in order for an RRSP to match a TFSA. If you make $1,000, you’re going to be left with $750 or so on your paycheque (because your employer deducted some tax, CPP, and EI from your bi-weekly payroll). In order for the RRSP to meet the TFSA in value in the end, you need to take the $250 refund generated from the RRSP contribution and contribute that to the RRSP as well.

If you want the refund to do some fun spending, consider the TFSA instead.

So, the key to maximizing the amounts in each account will come down to which tax rates you’re contributing at and which tax rates you’re withdrawing from — something only an adviser with knowledge of your particular situation will know.

Some Quick Tips

General recommendations for which savings plan to use is ill-advised — these are two investment tools designed for different types of earners. As I mentioned above, you’ll need to ask an adviser who has knowledge of your situation before getting a proper answer. (I’m happy to help! Shoot me an email.)

But there are some rules of thumb I recommend you understand. In no particular order:

RRSPs are a deferred income tool — just like pensions, just like rental properties, and just like cottages or small businesses. You can have too many deferred sources of income, resulting in extra-large amounts of tax to pay down the road when you sell the investment or when you withdraw cash from the RRSP account. If you are an employee who has an employer-sponsored pension plan, or if you have considerable deferred income sources already, consider utilizing the TFSA.

Conversely, if you are an earner who earns self-employment income or you are an employee with no pension plan or other deferred income sources, consider an RRSP. In effect, you can create your own pension plan inside an RRSP.

RRSPs are fantastic tools for tax sheltering windfalls of income in specific years. If you have taxable real estate such as rental properties, farmland, or a family cottage that will require tax be paid upon disposition, you can use an RRSP to shelter that windfall of income when it arrives. You cannot use a TFSA for this sort of windfall.

You can contribute to an RRSP up to December 31st of the year you turn 71 years old. If you foresee great amounts of deferred income upon death, you have a few options to absorb the tax impact: you can purchase a life insurance policy; or you can maximize your RRSP contributions, not deduct the RRSPs immediately, and use the contributions as a deduction on your final tax return. Talk to an adviser about this one.

To my way of thinking, the advantages of having open RRSP contribution space for cash windfalls or for handling tax for your estate outweigh the incentive to receive a tax refund for each year you contribute. I myself lean towards thinking the TFSA is a better savings tool for most people, but “most” only means 51% of earners. It’s a toss up and it’s worth a conversation with your adviser.

The best portfolios have a combination of TFSA and RRSP investments. Like everything in life, a little moderation and a diversification of investments is the best path forward.

I appreciate you sticking around with me for the first 12 issues of Toonie Newsletter. I’m excited to finish off this course so I can better turn my attention back to writing this newsletter each week — it’s too much fun to ignore.

If you feel like being awesome, hit the share button below to share this with a friend or two.

I hope you have a safe, healthy, and prosperous week ahead.

JG