Building a Do-It-Yourself ETF Investment Plan

Building a Do-It-Yourself ETF Investment Plan

Using a little tech and a simple savings plan, you can build a no cost, 100% controlled, and completely balanced portfolio of your own.

Good Friday morning everyone!

For my Canadian readers, I hope everyone had a great shortened week after Thanksgiving Monday. And for my international readers, I hope you look forward to your respective Thanksgivings or any other holidays that approach on your calendar.

Exciting times for me: Today begins one of the last chapters in my CPA designation pursuit.

Which also means I'll have that much less time to devote to everything else.

Don't fret though — there are a few issues I've put together to have on the back-burner for times like these, so I hope to still be invited into your inbox for a few weeks to come.

And as always, please shoot me an email if you have any questions, concerns or feedback.

This week, we look at the last major step in the "Where Do I Start?" 4-step plan. Once you have today's step setup and firing on its own, you can branch out into any investment direction you want.

Quick Thought of the Week

I never understood "minimum charges" or high hourly rates when I first entered the work force. "$150 per hour?! That's so much money!" I used to think.

But there's a lot you have to price into your time, especially as a creative freelancer.

You have to pay for your tools, which has to be spread across your clientele. You have to pay for your education or professional development. You have services, software, and physical supplies to include. And you have to pay yourself.

$150 per hour isn't an overly high hourly rate. I don't think you need to feel guilty to charge the amount you need in order to keep your world spinning.

Link of the Week: Stripe: The Internet's Most Undervalued Company

Though I feel like the author is reaching in some areas to justify Stripe's great positioning in the financial-technology sector, there is a lot to digest here and a lot to be excited about with this company. I found this summary of Stripe's history to be interesting:

While running Auctomatic, the Collisons realized that, despite PayPal’s success and banks’ participation, accepting payments online was too hard. They felt that with more businesses starting online, engineers would decide which payment tools to use, not finance people, and built a product that engineers loved. To this day, everything from their products to their communications are designed to delight engineers.

"They felt that with more businesses starting online, engineers would decide which payment tools to use, not finance people, and built a product that engineers loved."

How many other industries would be better served if people like me didn't build them out? Interesting point here.

A Do-It-Yourself ETF Investment Plan

First off, congratulations! If you're reading this and fully enacted the first three steps of the "Where Should I Start" plan, then you're well on your way to building the backbone of a successful financial career.

Step 1 was paying off your high interest debts without forgetting the power of saving as early as possible.

Step 2 was setting aside enough cash in an emergency fund to make it through two or three months if the worst takes place.

Step 3 was saving as much cash as possible for purchasing as big a home as you could possibly afford. Which is risky, to be sure, but it'll provide some stability as you enter into the fourth step in this simple plan.

Step 4 is all about branching out and away from your sole investment after step 3: your home. Diversification is the key to limiting risk in your investments and savings, and so it's only wise to buy all sorts of different assets as you grow over time.

I have a pretty quick and easy plan I recommend to young investors that includes the latest app technology and a no-fee way of accumulating assets that are spread out across the entire stock and bond market.

First though, some background and some reminders.

Reminder 1: Continue Growing Your Emergency Fund

Remember that pesky emergency fund? The cash account that was impossible to save and equally more difficult to look at as it sat there, depreciating in value each year?

Well, you're going to have to continue to increase the size of that account while you grow out your asset and investment portfolio. As your lifestyle changes, improves, increases, etc., you're going to need more cash to fund that lifestyle if disaster strikes.

Continue throwing enough into that account to at least overcome the cost of inflation (1.5% to 2% per year, in my mind).

Reminder 2: Remember Risk, Balance, and Control

I've touched on these briefly in a previous issue, but there are three pillars to growing an investment portfolio that you should consider.

Risk

"High risk, high reward." You've heard this before, for sure. "High risk, high probability of loss" is equally appropriate. The greater amount of risk you take, the more you could make and the more you could lose. Nearly guaranteed, the riskier you want to be, the more volatile your portfolio will behave.

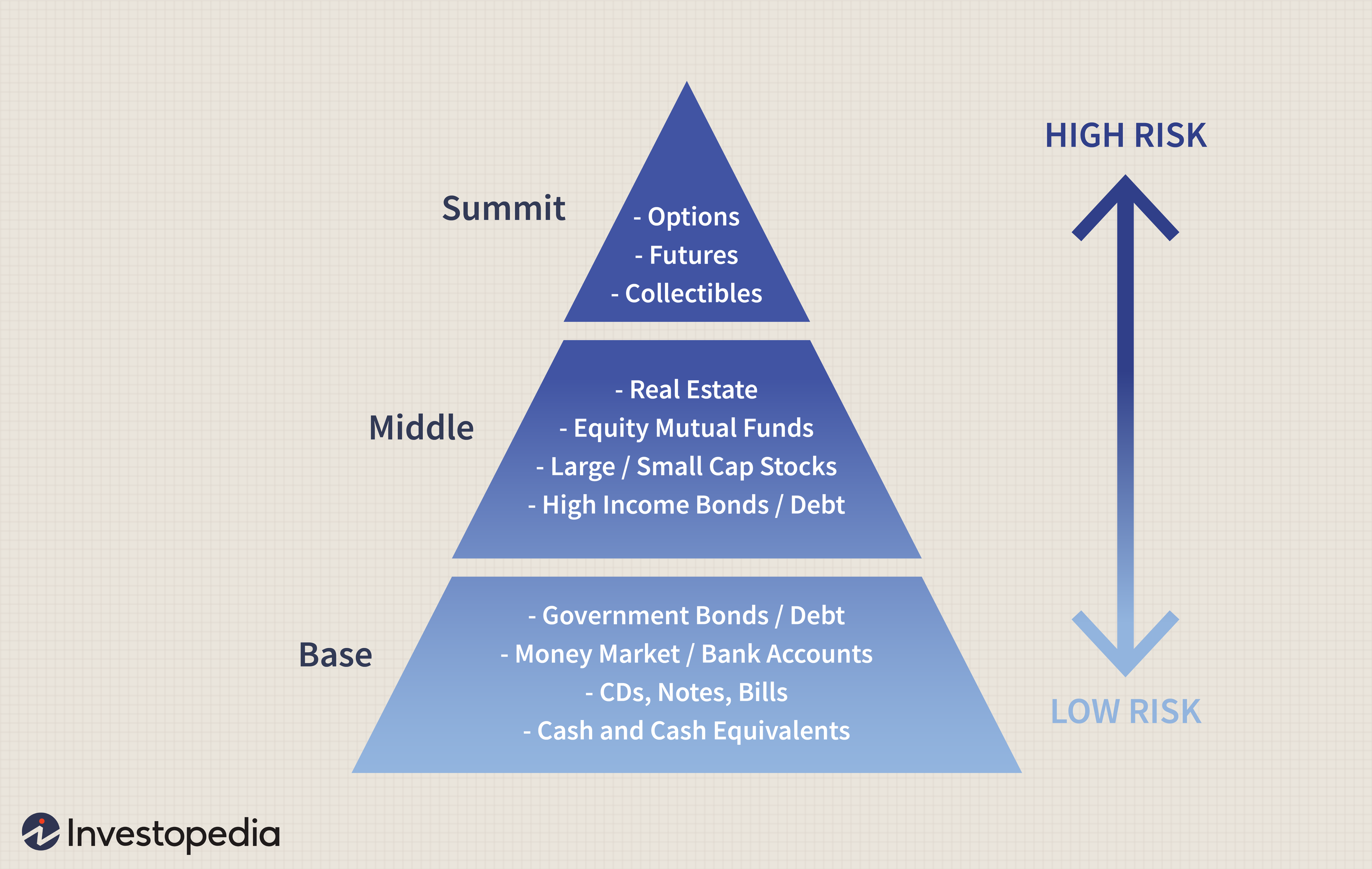

There are many, many variables to risk that can be quantified and qualified. But today's "risk continuum" is pretty simply explained in the following diagram:

Image taken from Investopedia.

You'll quickly notice government bonds and money market accounts are the least risky types of assets in this continuum, while equities, large and small cap stocks, and real estate take the middle of the continuum.

Where you fall in this risk continuum is largely up to your own personal preference, but a couple quick rules of thumb that I think are wise include:

Start with low-to-high risk and broad coverage assets (such as ETFs, much more on this in a bit) to build yourself a foundation that doesn't falter or sway too much.

The younger you are, the more risky you can act. Quite simply, the younger you are, the more time you have to recover any losses from previous years.

Balance

You can take "Balance" to mean two things.

First, "Balance" can mean a balance of all sorts of assets in your portfolio. I don't think it's wise to load up only on options and collectibles. I don't think it's wise to only load up on real estate, or only on government bonds, or only on cash.

I think it's tremendously wise to have a little bit of everything.

In this form, "Balance" can be taken as "Diversification" and you wouldn't be wrong in interpreting it this way.

Second, "Balance" can also mean "Don't focus every ounce of your energy on building your portfolio". I genuinely mean this — you don't die and take any money with you to the grave.

If you, like me, find wealth to be an incremental and slow process, then you have to remember to live life along the way too. If you have purchased assets that grow each day, if you have plans in place that are working steadily to achieve your long-term goals, and if you find comfort in the process, the next best thing to do is to actually spend some of your money.

This has lifestyle, estate, and tax implications, for whatever it's worth.

Lifestyle-wise, once you've put a plan in place, any extra can fund the occasional nicety in life. (Not too many, of course! But some seems OK in my mind.)

Estate-wise, any money given to your children while you're alive is money they won't receive after you die. Which should also be fine, given you are around and have some wisdom for your children on how to use the money wisely.

And tax-wise, if you leave tax-deferred money in your portfolio for too long, you'll run into an exorbitantly expensive tax bill on your deathbed. Getting that money into your income and into some after-tax personal assets is not the worst idea in the world.

All told, "Balance" should mean "Live a little, on occasion" as much as it means "Diversification".

Control

Like risk, there's also a control continuum. The more control you have over your own assets, the more risky your asset purchases are likely to be. Consequently, you'll pay less fees to an advisor to handle your investments for you.

Oppositely, the less control you have over your investments, the broader and more diversified your assets are likely to be, the less risky your investments are likely to be, and the more you'll pay to a manager to handle your investments.

This control and risk dichotomy has had a very long history, and it's one the greatest investor in history has taken a firm stance on. If you jumped into Berkshire Hathaway's 2016 Annual Report, you'll read Warren Buffett's now-famous remarks regarding the cost of hedge and mutual fund managers and how they outweigh the returns generated. Instead, Buffett believes the average investor is better off investing in low-cost index funds. Buffett (on page 23 and 24, if you're interested):

A number of smart people are involved in running hedge funds. But to a great extent their efforts are self-neutralizing, and their IQ will not overcome the costs they impose on investors. Investors, on average and over time, will do better with a low-cost index fund than with a group of funds of funds. Over the years, I’ve often been asked for investment advice, and in the process of answering I’ve learned a good deal about human behavior. My regular recommendation has been a low-cost S&P 500 index fund. To their credit, my friends who possess only modest means have usually followed my suggestion. I believe, however, that none of the mega-rich individuals, institutions or pension funds has followed that same advice when I’ve given it to them. Instead, these investors politely thank me for my thoughts and depart to listen to the siren song of a high-fee manager or, in the case of many institutions, to seek out another breed of hyper-helper called a consultant.

Don't be the "polite" individual and ignore Warren Buffett. Take his advice, and implement it as follows.

A Do-It-Yourself No Fee ETF Investment Plan

I'm no genius, and there are loads of folks out there who have implemented this simple plan for getting started on their post-home-acquisition investment portfolio. It's super simple:

Open an account with a no-fee trading platform. You can look at Questrade, where you can purchase ETFs commission-free. But I'm more inclined to recommend Wealthsimple Trade these days. Wealthsimple Trade has no fees to buy or sell ETFs and individual stocks. Wealthsimple only makes money in Trade through foreign exchange fees, which you're going to pay at any trading institution in Canada, no matter what.

Inside Wealthsimple Trade (or Questrade, or whichever no-fee platform you found), open a TFSA or an RRSP account. This question has huge implications and I don't have enough time to dive into it today. In short, open an RRSP account if you don't have an employer pension plan, if you earn a high salary (I'm thinking at least $90,000-$100,000 CAD or more), or ifyou believe you'll have significantly less income in your retirement than you do currently. Otherwise, open a TFSA. You should lean towards opening a TFSA no matter what.

Create a cash saving plan to put an amount your comfortable with from every paycheque you receive into your Wealthsimple Trade account. For me, this is $150 every 2 weeks. It's not a huge amount, but it's not nothing. Some back-of-the-envelope math suggests $5,000 per year at 6.62% (the average return of the Toronto Stock Exchange since 1988) compounded annually for 40 years will result in a portfolio of $965,400. Not bad for a simple $5,000 per year investment.

Purchase the same boring ETF over and over and over until you want to try something new.

Purchasing the Same ETF Over and Over

First, an ETF is an "exchange traded fund". The definition, from Investopedia:

An exchange traded fund (ETF) is a type of security that involves a collection of securities—such as stocks—that often tracks an underlying index, although they can invest in any number of industry sectors or use various strategies. ETFs are in many ways similar to mutual funds; however, they are listed on exchanges and ETF shares trade throughout the day just like ordinary stock.

In my words, an ETF is a collection of a wide range of stocks from an entire market or from a specific industry, of which you can purchase a tiny, tiny sliver in the form of a share of the ETF.

The key here: An ETF is a security that is traded and listed on a normal stock exchange (which means you can buy them yourself, unlike mutual funds), and ETFs have significantly lower costs than mutual funds.

To play this do-it-yourself ETF game, I recommend finding an ETF that has wide coverage of a wide range of assets across the entire world. And in Canada, there are at least three companies who offer these simple "All-in-One ETFs" that are perfect for the first step of your investment portfolio. From Million Dollar Journey (one of my favorite personal finance and investing blogs):

The basic idea is that some of Canada’s largest ETF providers decided that they didn’t want the robo advisors having all the fun when it comes to super simple investing solutions for the average Canadian. One of the big value propositions of a robo advisor is the idea that a couch potato investor (aka index investor, passive investor, etc.) no longer had to worry about rebalancing their various types of ETFs. Gone were the days of doing a little math to figure out if you were still hitting your asset allocation targets when it came to bonds, Canadian equities, and international equities. It was the new era where you just put your money in one place, and let the automated solution do the work for you. So Vanguard, BMO, iShares, and most recently Horizons ETFs put together products that are basically a few different ETFs, inside of a big umbrella ETF.

I've had a great amount of luck with Vanguard ETFs in the past, and so I'm biased towards any of Vanguard's All-in-One ETF options. Picking which one to constantly buy should depend simply on the amount of time you're planning on investing for:

Vanguard Conservative ETF Portfolio (VCNS): For investors looking to cash out of the market in 5 to 10 years.

Vanguard Balanced ETF Portfolio (VBAL): For investors looking to cash out of the market in 10 to 20 years.

Vanguard Growth ETF Portfolio (VGRO): For investors who are cashing out beyond 20 years of time.

Basically, pick a theoretical time way out in the future on when you want to retire and pick the corresponding ETF. Every two weeks, when your paycheque rolls into your account, funnel the amount of money you're comfortable with (first into your emergency fund) and then into your Wealthsimple Trade account.

And then purchase that same ETF over and over and over.

It won't cost you a thing to buy any of these ETFs if you use Wealthsimple Trade. It won't cost you a thing to sell them later on either.

And these ETFs will provide a healthy, broad, and diversified set of stocks and bonds in Canada, the United States, and emerging markets around the world.

When you find yourself getting into that 10 to 20 year timeframe, you can sell all your holdings and transition them into an ETF like VBAL instead.

A Roundup of the DIY ETF Portfolio

This simple plan won't cost you a thing (other than the fees baked into the ETFs themselves, which are very low overall), will provide broad coverage to assets throughout the entire world, and should result in returns greater than standard index funds (as mentioned by Warren Buffett) in the long, long term. Were I starting out again, these ETFs would 100% be the route I'd take (they weren't around when I started).

This plan provides a low risk method to owning a diverse set of stocks and bonds, provides you complete 100% control with little to no cost, and provides you ample balance by ensuring you don't need to save every extra dollar of your paycheque.

As you feel comfortable with where your simple DIY ETF portfolio is headed, you can start to take some of the cash you've saved and increase your risk tolerance by picking other ETFs or picking specific companies yourself. This DIY ETF portfolio will create a strong backbone and foundation to your investment portfolio, and the rest you can have fun with.

So, in summary:

Open a Wealthsimple Trade account.

Transfer money into it every paycheque.

Purchase the same Vanguard (or competing company) ETF over and over and over.

Thank you greatly for working through this 4-step process answering the "Where Do I Start?" question. If you have some advice for me, or if you have questions, fire me an email and let's chat. There are so many smart folks out there and I'm always interested in learning.

Now that you know all my starting out secrets, feel free to forward these links to anyone who asks you the "Where Do I Start?" question.

Step 4: Building a Do-It-Yourself ETF Investment Plan

I hope you and your family have a fantastic weekend and a productive week ahead.

JG