A Trick for Saving Interest on Your Mortgage and to Pay Off Your Mortgage 3 Years Sooner

A Trick for Saving Interest on Your Mortgage and to Pay Off Your Mortgage 3 Years Sooner

An automated payment and transfer schedule has cut our interest cost down significantly in the long-term.

Good Friday morning friends!

Depending on where you know me from, you may already know that I'm a bit of a Star Wars nerd. I confess to re-enacting major Star Wars lightsaber fights well into my teenage years.

That love for a galaxy far, far away has never subsided.

Though I haven't read a single spoiler, it's quite likely tomorrow marks one of the most consequential Star Wars TV episodes to ever hit the airwaves. As I write this Thursday night, I'm considering waking up at 2:00AM to take in the latest episode of The Mandalorian.

If you're even half a Star Wars fan, I implore you to watch The Mandalorian on Disney+. The first season moves slow, but it builds a live action world we haven't properly seen since the 1970s. And this second season seems to be firing on all cylinders.

Again, watch it if you even kind of want to. It's worth your time.

Now, some financial talk. This week: college degrees, a millennial doctor who spends $15,000 a month, and a previously written trick for saving some interest expense on your mortgage.

Quick Thought of the Week

I've read many articles in recent years discussing the diminishing value of a post-secondary education. In an increasingly gig economy and a world of technological disrupters learning how to change the world in their basement rather than in the classroom, the idea of a diminishing college education value makes a lot of sense.

But that "value" has to be measured on a base. The less you put into something and the more you get out, the greater the value of that investment.

So when I say the government pays for the better part of 60% of post secondary degrees today, would that sway a person into thinking there's still great value in a college education?

Canadians who attend a recognized post secondary institution receive both federal and provincial tax credits for tuition paid and for "textbook" amounts paid (tax law doesn't change as fast as iPads evolve). This amounts to 25% coverage of your tuition and books cost depending on the province you live in.

You can claim rent credits in many provinces for rent paid out to attend post secondary.

If you're the beneficiary of an RESP, the government has already kicked in 20% into your college fund.

And depending on your province of residence, there may be tax credits available after you graduate.

This doesn't include grants paid to the universities to keep the overall costs lower for all students in attendance.

Finally, depending on the industry you enter into, that college education may result in an annual pay increase of $20,000 to $50,000 per year (or more!), and that increase generally lasts throughout your working career.

All told, I'm not entirely convinced the day of the college degree is over. You certainly don't need a college degree to make your world spin around in healthy finances, but it'd be foolish to state a college degree is a waste of money.

Link(s) of the Week

I was planning to share the Million Dollar Journey link all week until I came across the second eye-popper from the Financial Post. At this point, I recommend checking into the Financial Post regularly — there are some great columns published there each week.

Canadian Railway Dividends: Putting Your Portfolio On the Right Track — Million Dollar Journey

For you investors out there looking to expand your portfolio diversification, one of my favourite bloggers makes the case to add one of the five Canadian wide moat companies to your list:

While having a lock on a sector is an obvious benefit and it removes the risk of competition, it is no guarantee of investment success. There can be periods of weakness. The railways are economically sensitive companies. When the economy slows, less goods are moved around the country. In a recession, rail traffic can be greatly impaired.

For example, in the not-too-distant past, the rails were moving a lot of oil, but those volumes have dropped due to the pandemic. Much of that oil supply has moved back to the pipelines. So if you also hold some of the major pipelines in Canada you’ll be picking up that business by way of those holdings.

Though the pipeline company I own (Pembina Pipeline) has had a rough year, it seems like it's on the mend right now (along with the rest of the market).

Either way, I had never considered a Canadian railway before. Now, they're right at the top of my list.

This millennial doctor pulled in $40K one recent month, but his wild spending ways may catch up to him — Financial Post

My eyes popped out of my head when reading this piece about a young doctor who makes a ton of money and spends a ton of money to boot. Normally Spent highlights folks who work sub-$100,000 jobs attempting to save for a major financial goal somewhere down the road.

This week's Spent comes at things from an entirely different angle.

A Trick for Saving Interest on Your Mortgage and to Pay Off Your Mortgage 3 Years Sooner

Note: This post was originally published on The Newsprint.

One of the easiest tricks in the book to pay off your mortgage faster is to make bi-weekly payments instead of monthly payments. Any mortgage calculator will show this and, since most people are paid bi-weekly, it makes a lot of sense to match your mortgage payment schedule to your income schedule.

Here’s another method my wife and I are using to pay down our mortgage quicker:

In short:

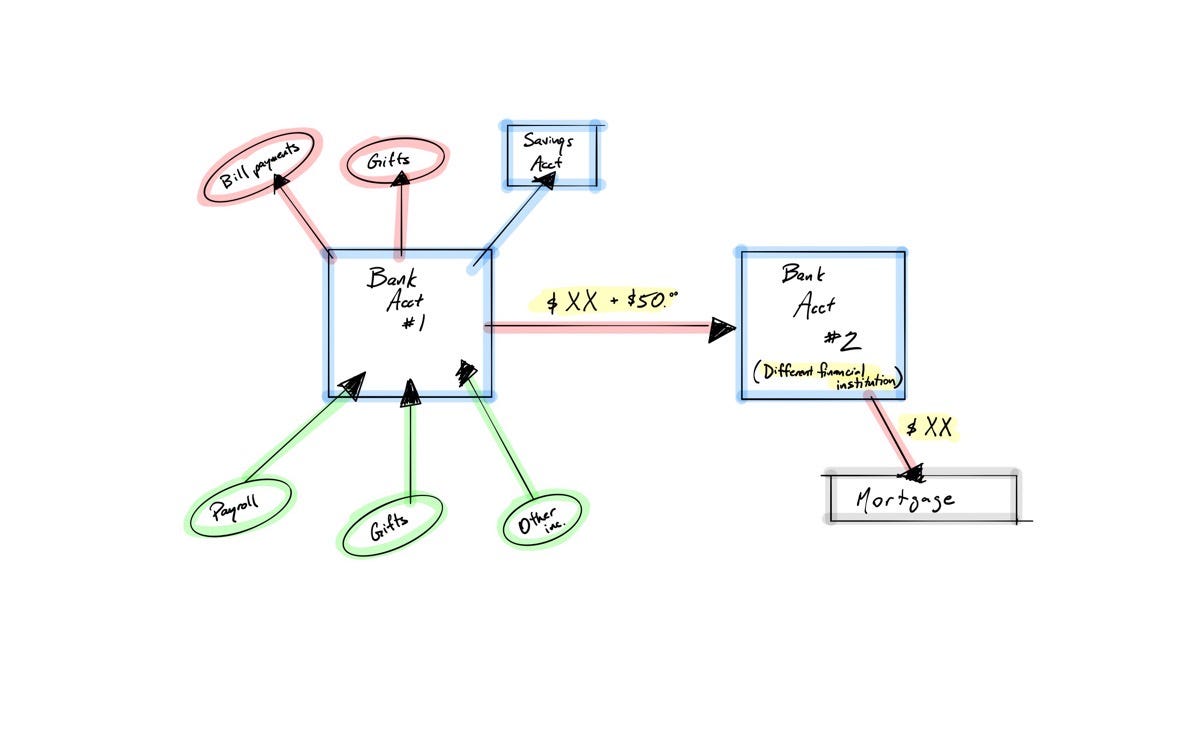

Everything flows into our main bank account: payroll, other income, gifts, etc.

That same bank account makes all the bill payments, all the transfers, etc.

Our mortgage is held at a different financial institution than our “operating” bank account.

The mortgage is paid out of a bank account held at the same institution as the mortgage.

Transfers are made every two weeks from our operating account to the “mortgage” bank account.

Our mortgage bank account is not easily accessed; we do not have a debit card for the account, we do not have quick or easy online access on our phones to the bank account, and the bank account has usage fees if we complete any transactions other than mortgage payments.

Based on the graphic, you can probably figure out the rest of the story. Our mortgage payment is $XX and is paid out of the mortgage bank account every two weeks. The transfer we make from our operating bank account to the mortgage bank account is $50 more than the required mortgage payment. And all these transfers are pre-authorized transfers which require signatures and paperwork to change.

After a year, it’s easy to see how a balance of $1,300 builds in that mortgage bank account. At the end of the year, we take the $1,300 and make an extra, principal-only mortgage payment. And then we start all over.

On a $250,000 mortgage, this additional $50 in the bi-weekly transfer dramatically cuts down on interest costs in the long run. As per the Government of Canada’s Mortgage Calculator, the $1,300 additional annual payment results in (assuming a 3% interest rate on a 5-year term amortized over 25 years):

Savings of $13,191.55 in interest costs over the course of the mortgage.

Mortgage payoff 35 months sooner.

Savings of $407.52 in interest costs over the course of the first 5-year term.

“OK, Josh. Great idea,” you say.

“But why not just make your mortgage payment higher? Clearly you can afford more.”

Aha! Great question.

The point with this trick is that you are locked into a lower required cash outflow on a bi-weekly basis than if you made larger mortgage payments. Larger mortgage payments will pay off your mortgage faster and will result in greater interest savings in the long run, to be sure.

However, should a crisis strike, having a lesser required cash outflow may be nice to have. That extra $1,300 is exactly that: extra. It’s not required. You could use the $1,300 and invest it in the stock market. You could save it in a Tax Free Savings Account and use the money to purchase an investment property down the road. If you have children, you could put the money into a Registered Education Savings Plan and receive the 20% RESP governmental grant on top of it.

Whatever you choose to do with the $1,300 is up to you. Extra mortgage payments simply provide a guaranteed return.

I was updating all our personal finances the other day and completely forgot about the fact that we have an extra $50 transferred every two weeks. Seeing the accumulated balance was a nice little revelation; there’s nothing quite like the rush you get when you stumble across “found money”.

And I figured, perhaps, this could help some other folks to get ahead of their mortgage a little quicker.

Thanks for reading this week. If you feel like being awesome, hit this share button to spread the word.

And if you have any questions or concerns, I love receiving emails.

Have a safe and healthy weekend and a prosperous week ahead.

JG